The Evolution of the ODA Accounting Rules

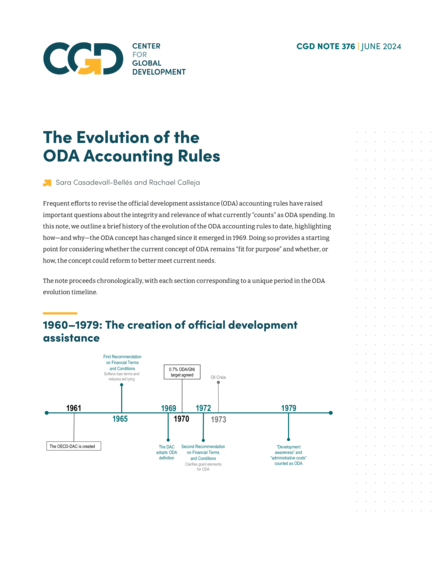

Frequent efforts to revise the official development assistance (ODA) accounting rules have raised important questions about the integrity and relevance of what currently “counts” as ODA spending. In this note, we outline a brief history of the evolution of the ODA accounting rules to date, highlighting how—and why—the ODA concept has changed since it emerged in 1969. Doing so provides a starting point for considering whether the current concept of ODA remains “fit for purpose” and whether, or how, the concept could reform to better meet current needs.